Insights

What is RCS messaging? Google’s communication chat protocol explained

If SMS had been invented today, it probably wouldn’t be limited to 160 characters of plain text, and you wouldn’t need MMS just to send a picture. Instead, you’d probably end up with something a lot closer to Rich Communication Services (RCS), a messaging protocol built for the smartphone era with rich media, tappable buttons, branded messages for business messaging, and more.

So, what is RCS messaging, and why is it taking off now? RCS has been around for a while (since 2006, actually), but it’s now hitting its stride. With support from Android, carriers worldwide, and even Apple support in some markets, RCS is living up to its promise: making messaging smarter, more secure, and way more interactive.

So, what does that mean for your business? Better engagement and sales, more trust, and conversations that actually drive action – all in your customers’ native messaging inboxes.

What is an RCS message?

What does RCS mean? RCS stands for Rich Communication Services – a messaging protocol developed by the Global System for Mobile Communications Association (GSMA) as the evolution of SMS. An RCS text message is more than just a text – it’s an interactive, app-like experience delivered directly to your customer’s native messaging inbox.

An RCS message supports rich chat features like high-res images and videos, rich cards, suggested replies, branded sender information, and real-time indicators like “typing…” and “read.” Best of all, RCS messaging delivers these interactive experiences directly to a user’s native mobile messaging inbox on Android and Apple devices, meaning there’s no third-party app required.

So what is an RCS chat, exactly? An RCS chat is a conversation that takes place using the RCS protocol rather than traditional SMS. RCS chats offer communication capabilities like read receipts, typing indicators, and high-quality media sharing – and can also include multimedia like web pages, maps, and other images, all directly in a user’s native mobile inbox.

For users, RCS means better conversations. For businesses, RCS means you can deliver sleek, branded, app-like experiences straight to your customers’ native text inboxes. Think order confirmations with maps, product carousels, or even full two-way conversations with customer support.

And because businesses can struggle with getting users to download and regularly use their mobile apps, RCS can help reduce that friction by bringing app-like functionality directly into the messaging experience. Want to understand the full picture of how messages flow? Check out our deep-dive on how RCS works.

In 2025, RCS had over one and a half billion monthly active users, and its reach is still growing in 2026, thanks to expanding support by Apple and mobile operators.

Sinch’s Robert Gerstmann said that one of the potential powers of RCS is that it can replace apps altogether. While that may sound radical, it’s possible. Many of the most common uses of apps (checking balances, placing orders) could be handled with rich messaging.

Plus, the process for a company to get verified to use RCS builds consumer trust, making them more likely to engage on that channel.

In our 2025 State of customer communications survey of 1,600 business leaders, nearly 87% of business leaders across industries were already familiar with RCS. Tech leaders (71%), healthcare (56%), financial services (55%), and retailers (53%) called it game-changing for customer communications.

Is RCS chat only for Android phones? Does Apple have RCS messaging?

For years, RCS was largely an Android experience. That shifted in 2024 when Apple introduced RCS support in iOS 18 for person-to-person (P2P) messaging, starting in select markets with carriers like AT&T, T-Mobile, and Verizon.

Apple has continued to widen their support and eventually began rolling out the application-to-person (A2P) version of RCS, known as RCS for Business (formerly “RBM”) with certain operators.

In 2025, Apple rolled out iOS 26, which brought broader updates that shape how people receive messages and calls. Features like filtering unknown senders, a dedicated SMS spam folder, and priority handling for time-sensitive messages give users more control over what they see.

Apple also confirmed support for RCS Universal Profile 3.0, the industry standard for RCS that standardizes RCS features across devices. When it happens, it will bring features like in-line replies, editing, unsending, and end-to-end, cross-platform encryption between Android and iPhone. However, this update is not yet available in iOS 26.

The rollout continues to move quickly. In March 2026, Apple released iOS 26.4, which includes testing for end-to-end encrypted RCS messaging – a significant step toward the cross-platform encryption that the GSMA’s RCS Universal Profile 3.0 has been working toward. This signals that full, interoperable E2EE between iPhone and Android is getting closer to reality.

In short, RCS is no longer an Android-only channel. As Apple expands support and more carriers adopt RCS messaging, more and more businesses will be able to reach customers with messaging that’s more interactive, trusted, and effective – no matter what phone they use.

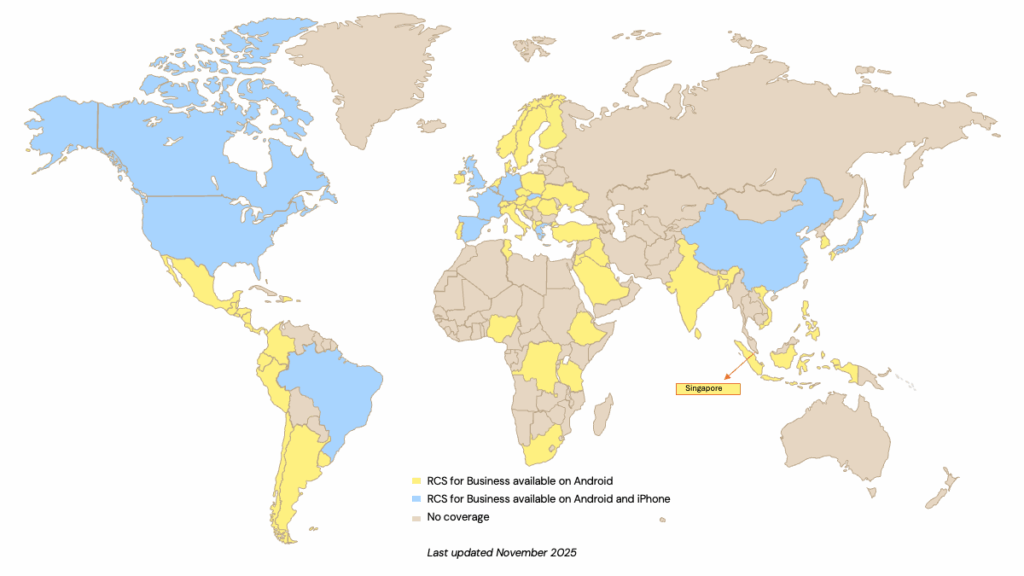

Where is RCS messaging used?

RCS has full coverage in Canada, Mexico, Brazil, the U.K., Germany, France, Spain, Italy, and India. Other countries offer full support via Google’s RCS services or partial support, with a selection of local mobile operators providing RCS.

When it comes to RCS for Business, coverage depends on a mix of mobile carrier support and regional rollout, especially as Apple gradually expands availability.

Here’s the kicker: Android accounts for over 79% of the global smartphone market. So even if you’re waiting for full iPhone support in your region, there’s already a massive audience you can reach today with rich, branded messaging that goes far beyond what SMS can do.

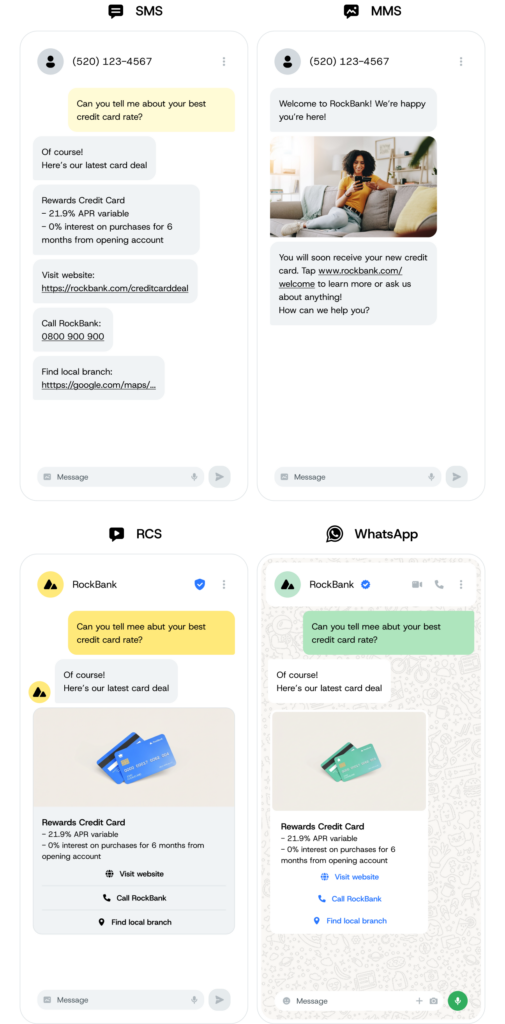

RCS vs. SMS, MMS, and OTT messaging apps

To understand the differences between an RCS message and text messaging, it might be helpful to first understand the differences between MMS and SMS.

While SMS is simple and reliable, it’s limited to 160 characters per message. MMS messages add the ability to send multimedia attachments, but RCS offers a much more interactive user experience.

And that’s because RCS messages work with other elements of a smartphone, like a web browser or maps, to create way more engaging conversations.

Is RCS going to replace traditional SMS? Not exactly. RCS runs on a mobile data connection or Wi-Fi, meaning SMS will still kick in when there’s no internet – just like iMessage will fall back to SMS when needed.

| SMS | MMS | RCS | iMessage | ||

| Network | Cellular network | Cellular network | Mobile data or Wi-Fi | Mobile data or Wi-Fi | Mobile data or Wi-Fi |

| Content | Text only (160 character limit) | Text and basic media (images, video, audio) | High-quality media, rich content, carousels, GIFs, and more | Text, high-quality media, GIFs, stickers, and more | Text, media, documents, voice messages, and more |

| Features | No typing indicators or read receipts | No typing indicators or read receipts | Typing indicators, read receipts, suggested replies, group chats, and more | Typing indicators, read receipts, reactions, editing, unsending, group chats | Typing indicators, read receipts, reactions, group chats, and more |

| App required? | No – native messaging inbox | No – native messaging inbox | No – native messaging inbox | No – native to iPhone/Mac/iPad | Yes – separate app download required |

| Business messaging | Basic A2P; no branding | Basic A2P; no branding | Verified sender, branded profile, rich interactive messages | No native A2P business messaging | WhatsApp Business API; branded profile |

| Encryption | None | None | In-transit encryption; E2EE in testing (iOS 26.4) | End-to-end encrypted by default | End-to-end encrypted by default |

| Availability | Universal | Universal | Android + iPhone (iOS 18+, carrier dependent) | Apple devices only | Requires app install; ~3 billion users globally |

RCS vs. SMS

SMS is simple and reliable, but limited to 160 characters per message with no support for rich media, read receipts, or typing indicators. RCS removes all of those limitations, delivering an interactive, app-like experience directly in the native messaging inbox – no download required.

RCS runs on mobile data or Wi-Fi, so SMS will still kick in as a fallback when there’s no internet connection.

RCS vs. MMS

MMS messages add the ability to send multimedia attachments like images and short videos over the cellular network, but the experience is basic. RCS offers much higher resolution media, larger file sizes (up to 100MB), carousels, suggested reply buttons, and two-way conversational features that MMS simply can’t match.

RCS vs. iMessage

iMessage is Apple’s proprietary messaging platform with end-to-end encryption and rich features – but it only works between Apple devices. RCS is an open standard that works across Android and iPhone, making it the cross-platform alternative.

With Apple’s adoption of RCS Universal Profile 3.0, interoperable end-to-end encryption between Android and iPhone is also on the horizon.

RCS vs. OTT messaging apps

Unlike over-the-top (OTT) apps like WhatsApp or Facebook Messenger, RCS doesn’t require users to download anything or create a new account. RCS works within the native messaging app built into different devices.

Exciting RCS features that set it apart

What does RCS do better than SMS? Well, just about everything! To see the full range of what’s possible, explore the different types of RCS for Business messages. Where SMS is limited to plain text and links, RCS offers features like:

- Better security: RCS messages are encrypted in transit, and in some cases, like RCS chats in Google Messages, they’re protected with end-to-end encryption.

- Higher text limits: SMS messages are limited to 160 characters, while text portions of RCS messages are limited to 3,072 characters.

- High-resolution images and videos: Grab attention with gorgeous high-resolution photos and videos, GIFs, carousels, and other dynamic features right in the native messaging app.

- Larger file sizes: Send images and videos up to 100MB (though Google recommends images up to 2MB and videos up to 10MB for the best experience).

- Message reactions and typing indicators: Just like in modern messaging apps, RCS supports reactions (like thumbs up or hearts) and shows when someone is typing. These features are available on both Android and iOS, and for cross-device messaging.

- Read receipts: If the recipient has their read receipts enabled, you’ll see the word “Read” along with the time they read your RCS message.

- Cross-app connectivity: Send messages that open in browsers, maps, and other applications.

- Easy, one-tap replies: RCS for Business messages make it easy to reply to messages with one tap with suggested replies.

- Group chats: Connect securely in group messages with friends, family, and team members without requiring another chat app.

- Google Wallet integration: Provides a quicker and easier way to access everyday essentials.

Why RCS for Business is a game-changer for your company

RCS lets you build more engaging content and provide a better customer experience for those with RCS-enabled devices. Time and time again, RCS for Business has been proven to lead to higher cart values, more conversions, and higher engagement than any other type of mobile messaging.

“One of the cool things about RCS is that you can do so much with it. A lot of businesses start with fairly simple messages, by converting their existing SMS over. That works well for improving security with the sender verifications, the branding, and the delivery receipts. And once you start seeing it working, you start to move on to more advanced use cases.”

Once you’re verified and live, here’s what businesses love most about using RCS:

Enhanced branding and trust

In our 2025 State of RCS in customer communications report, 79% of consumers said logos and verification checkmarks make messages feel more trustworthy.

RCS messages display your business name, logo, and verified sender status so customers always know exactly who they’re talking to – making it ideal for sensitive messages like one-time passwords sent via RCS.

Boosted read and response rates

Because RCS messages land in the native messaging inbox with rich, interactive content, they consistently outperform SMS on open rates, read rates, and response rates.

Our 2025 State of customer communications research shows that 40% of business leaders believe RCS will increase customer engagement through its interactive features.

Elevated analytics and insights

Handset delivery receipts, open rates, and read rates give you more in-depth information about the status of messages. This makes A/B testing and campaign optimization easier – and more effective.

No extra downloads

All new Android devices have built-in RCS, so messages from verified businesses can go directly to the native messaging inbox instead of needing a separate app.

Rich, interactive features

From image carousels and videos to reply buttons and suggested actions, you can keep users engaged – and guide them toward the next step – without sending them elsewhere.

Explore the full range of RCS for Business message types to see what’s possible.

Reliable fallbacks

If someone doesn’t have RCS (or a mobile data plan to support it), your message can still be delivered as SMS, MMS, or apps like WhatsApp if you send via Sinch Conversation API or Sinch Engage.

In short, your messages will always get to your customers, one way or another.

How RCS messaging can grow your business (real-world RCS examples)

Like most other kinds of marketing and support, the ability to grow your business using RCS is only limited by your imagination and your budget. It’s good to remember just how powerful these messages can be – do you know any other form of outreach that’s as embedded in your customers’ daily routine as their text inbox? Neither do we.

Promotions and specials

Provide up-to-the-minute information on sales and promotions tailored to a customer’s tastes. With the added functionality of RCS, you can send them to your website, or give them directions to your location. You can even have them choose what they want and order it right from your message!

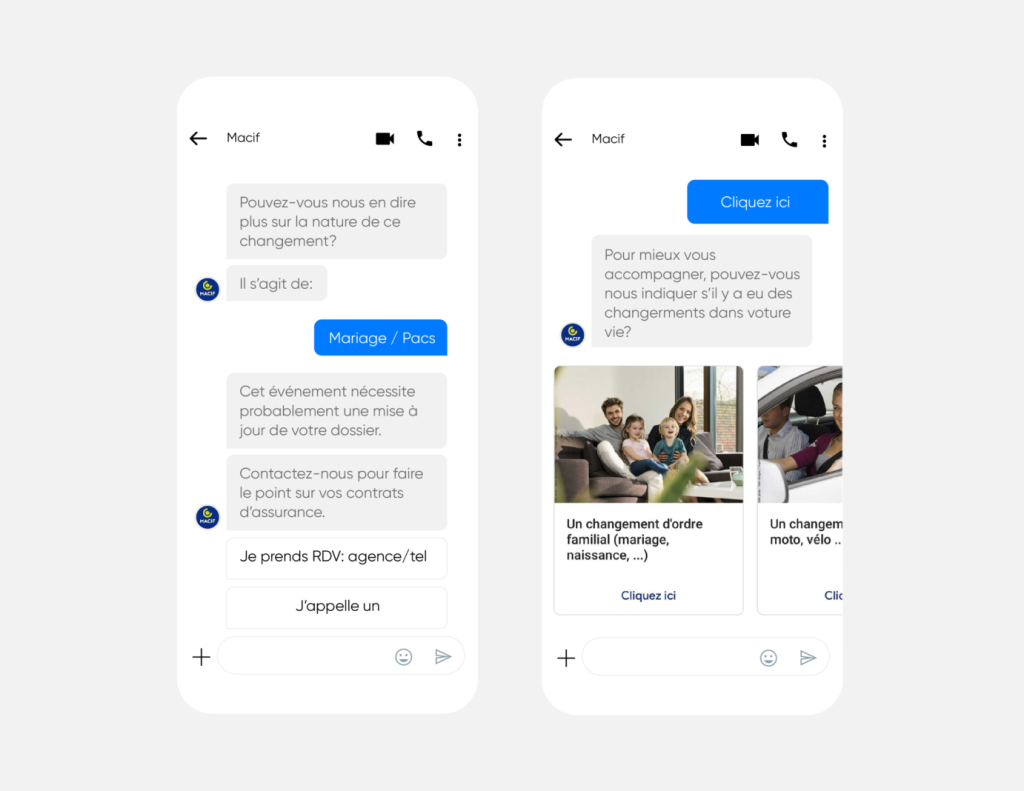

Here’s a real-life example: Macif, an insurance company with over five million policyholders in France, used RCS to have two-way conversations.

Real-time updates

RCS allows your customers to engage with a conversational service (including live support or AI chatbots), for instance, to schedule or change appointments. You can also provide directions, sports scores, and shipping updates as they happen.

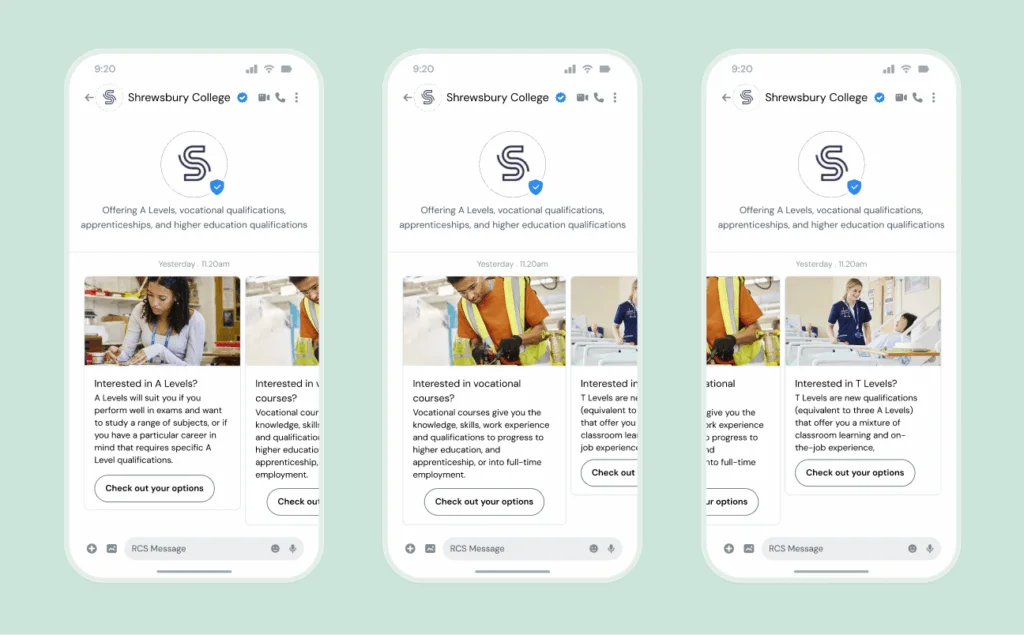

Here’s a real-world example from the education sector: Shrewsbury College, a leading UK education provider, uses RCS to send students interactive updates on enrollment and course information directly in their native mobile messaging app.

With automated SMS and RCS messages running through Sinch Engage’s HubSpot texting integration, the college boosted engagement, improved response times, and reduced administrative work across enrollment and student support.

Smarter account alerts

RCS takes traditional account alerts to the next level with verified sender information, branding, and more. Think branded fraud alerts, payment confirmations, or service reminders that land in your customers’ native text message inboxes.

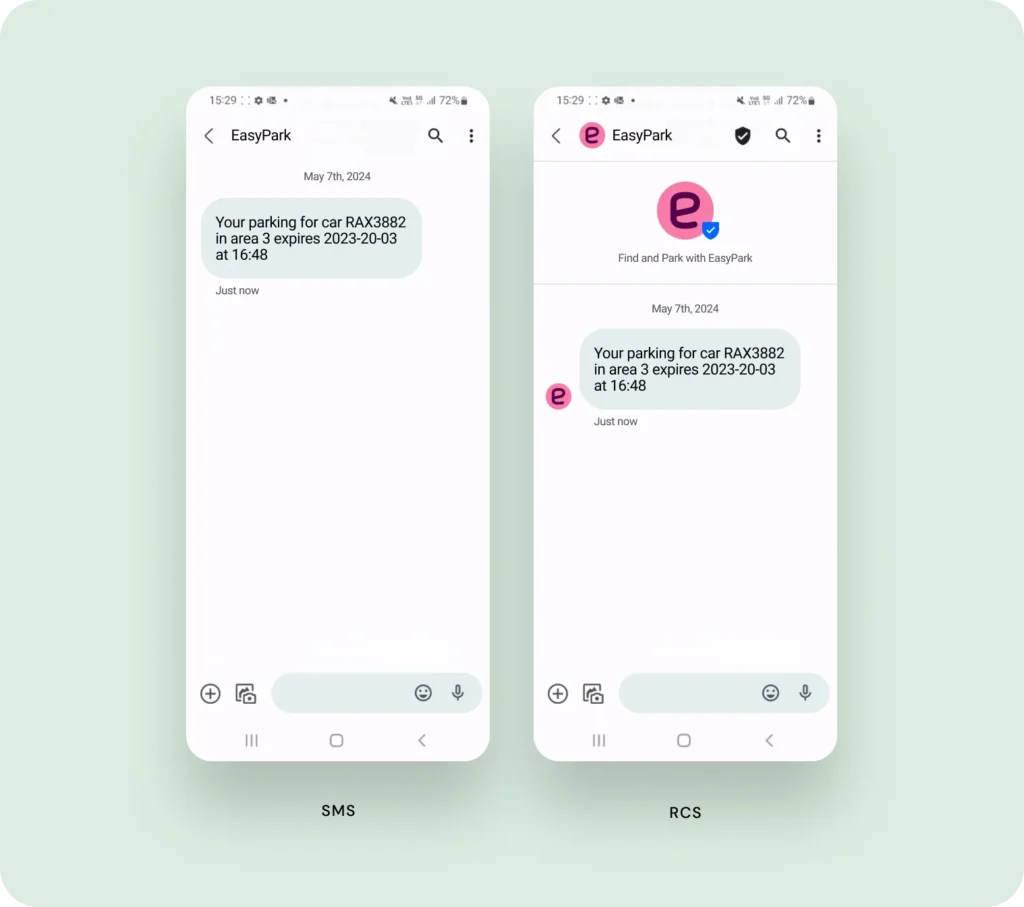

Case in point: EasyPark Group, the world leader in digital parking, uses RCS texts to send real-time parking alerts, complete with their logo and a verified check mark. If a user’s device doesn’t support RCS, it falls back to SMS automatically.

Personalized recommendations

Personalization is one of the most important parts of any communication or marketing strategy. In fact, in our 2025 State of customer communications consumer survey, 80% of consumers said they value personalized recommendations.

RCS makes personalized messaging feel like a conversation, especially when product suggestions are tailored to past purchases, preferences, or behavior. Here’s another real-world RCS messaging example at work: Picard used an RCS campaign to lift sales and win customer loyalty.

They created a conversational RCS experience that helped their customers imagine their holiday menus, taking into account dietary preferences, budget considerations, and even their desire to cook.

Their campaign achieved great results, with a 42% increase in customer engagement and 10% more website clicks than Rich SMS.

RCS chatbot best practices we learned from customers that use RCS for Business

One of the most powerful applications of RCS for Business is the chatbot experience – delivering automated, conversational interactions that feel personal and on-brand. Here’s how to do it right:

Be clear about what your RCS chatbot does

Set expectations upfront. Let customers know they’re interacting with an automated experience, what it can help with, and what topics are in scope. Clear framing reduces frustration and builds trust.

Provide an optimal experience

Use RCS’s rich features – suggested replies, carousels, quick-tap buttons – to make conversations as frictionless as possible. The easier it is for customers to take action, the better your results will be.

Always have a human fallback option

No chatbot can handle every situation. Always provide a clear path to a live agent, whether that’s a “Talk to a person” suggested reply or a handoff trigger when the bot reaches its limits.

Provide suggestions to steer users

Don’t leave customers staring at a blank text field. Suggested replies and action buttons guide users through the conversation and make it far more likely they’ll complete the intended action.

Ensure your chatbot reflects your brand

Your RCS chatbot is a brand touchpoint. The tone, language, and visual elements should all align with your wider brand identity.

Does RCS cost money?

For consumers, RCS messaging is free to use – it works over Wi-Fi or your mobile data connection rather than consuming SMS credits. However, it does require an active data connection, so if you’re on a limited data plan, RCS messages will use a small amount of data (though typically far less than browsing the web or streaming video).

For businesses using RCS for Business (A2P messaging), costs are similar to SMS in that you pay per message sent, though pricing varies by provider and region.

The good news: because RCS messages are more engaging and drive higher conversion rates, the ROI typically far exceeds that of SMS.

How to enable RCS messaging on your smartphone to experience it for yourself

Getting started with RCS is straightforward on both Android and iPhone.

How to enable RCS messaging on Android

All new Android devices come with RCS chat built in. Here’s how to turn it on in Google Messages:

- Open Google Messages on your device.

- Tap your profile picture in the top right, then select Message settings.

- Tap RCS chats.

- Toggle RCS chats on.

Note that you may need to verify your phone number before RCS is enabled.

How to enable RCS messaging on iPhone

If you have iOS 18 or higher and your carrier supports RCS on iPhone, you can enable it in your iPhone’s Message settings:

- Go to Settings > Apps > Messages.

- Tap RCS messaging.

- Toggle it on.

Once enabled, you’ll see “Text Message • RCS” in the message field when composing a message to an Android user, confirming RCS is active.

Getting started with RCS for Business

What’s the best way to start out strong with this exciting new channel?

- Research how others in your field are using RCS. Check out our RCS statistics to understand adoption trends by industry. If your competitors aren’t using the channel, take the plunge and get in on the ground floor of what’s almost guaranteed to become one of the most powerful tools in the upcoming years.

- Find and register your RCS Agent. An RCS Agent is your official business identity within the RCS ecosystem. Get started via Sinch RCS for Business via Conversation API or Sinch Engage, which you can also use to add other channels and scale as needed.

- Build a strategy. Use your data and previous messaging use cases to build better support, marketing, and sales processes. Sinch makes it easy to automate customer care and conversations for improved efficiency and better customer experience (CX). Our RCS marketing guide is a great starting point.

- A/B test your strategies. Once you’ve implemented new strategies, test them out. Start with a small group to iron out any major headaches and then expand. Capture as much data as you can to inform future decisions. Sinch Conversation API makes it easy to run multichannel tests at scale.

- Roll them out and refine them. Keep improving your strategies as you gain more experience and let customers tell you directly what they’d like to see in your messages.

As RCS messaging continues to gain ground, you can make great strides with this channel. And others already are! Download our free report backed by new global survey data about how businesses across different industries are using RCS messaging, and discover the strategies you need to stay ahead.

And when you’re ready to talk all things conversational messaging and RCS, let’s chat. Our team is ready to help you build a great messaging experience that your customers will love!

Frequently asked questions about RCS messaging

If you have iOS 18 or higher and your carrier supports RCS on iPhone, go to Settings > Apps > Messages > RCS messaging and toggle it on. Once it’s on, you’ll get a more modern experience when messaging Android users – including features like read receipts and typing indicators.

Open Google Messages, tap your profile picture, go to Message settings > RCS chats, and toggle RCS chats on. Note that you may need to verify your phone number before RCS is enabled.

RCS and iMessage are separate messaging services on iPhone. iMessage is used for Apple-to-Apple chats, while RCS is used for Apple-to-Android conversations when both carriers support it.

You cannot manually switch a conversation between iMessage and RCS, but your iPhone will choose the correct format automatically based on who you are messaging and what their device supports.

Yes. Apple continues to use blue bubbles for iMessage and green bubbles for non-iMessage conversations, including RCS chats with Android users. Even with RCS enabled, the color of the bubble does not change.

What does change is the experience inside the bubble – such as higher-quality media, typing indicators, and read receipts.

RCS supports many modern security features, including encryption for messages sent between Android devices. Apple has stated that interoperable end-to-end encryption for RCS between iPhone and Android is planned for a future update aligned with RCS Universal Profile standards.

Meanwhile, iMessage offers end-to-end encryption for P2P messages but is limited to Apple devices.

No. RCS requires an active data connection to send and receive messages. This can be mobile data or Wi-Fi. If you lose internet access, your conversation may fall back to SMS or MMS, depending on your device and carrier settings.

If one or more participants in a group chat don’t support RCS, the conversation will typically fall back to MMS for all participants to ensure everyone can receive the messages.

Yes. Apple has been rolling out support for RCS for Business (A2P messaging) with certain operators, and coverage is expanding.

Learn more about Apple’s RCS support or contact Sinch to understand availability in your target markets.

For consumers, RCS is free – it uses your mobile data or Wi-Fi connection rather than SMS credits. It requires an active internet connection to send and receive messages.

RCS Universal Profile 3.0 includes support for editing and unsending messages. However, availability of these features depends on the devices and carriers involved, as well as which version of the RCS standard is in use.

RCS (Rich Communication Services) is the next generation of mobile messaging, designed to replace SMS with a richer, more interactive experience. It supports high-resolution media, read receipts, typing indicators, suggested reply buttons, and branded business messaging – all delivered to a user’s native messaging inbox without requiring a separate app.

RCS stands for Rich Communication Services. It’s an open messaging standard developed by the GSMA that upgrades traditional SMS with modern, app-like features. Think of it as what SMS would look like if it were invented for the smartphone era.

An RCS chat is a conversation that uses the Rich Communication Services protocol instead of SMS. RCS chats support read receipts, typing indicators, high-resolution media, group messaging, and two-way interactive conversations – all within the native messaging app on Android or iPhone.

For businesses, RCS chats can include branded sender profiles, suggested replies, and rich content like carousels and action buttons.

An RCS text message is a message sent using the Rich Communication Services protocol rather than traditional SMS. Unlike a standard text, an RCS text message can include high-resolution images and videos, interactive buttons, carousels, read receipts, and branded sender information – all within the recipient’s native messaging app on Android or iPhone.

Author: